I had a nice conversation the other day with a research group about the future of cash. Here's a quick summary of the conversation.

The conversation explores the future of cash and digital currencies, highlighting different demographic preferences and the challenges in transitioning to a cashless society.

- Demographic Tiers: There are three main demographic groups: tech-savvy individuals who use cryptocurrencies, people who prefer stable coins and government-issued digital currencies, and those who only trust physical cash.

- Cash Trust and Anonymity: Cash is trusted because it is anonymous, and there are few digital equivalents that offer the same level of anonymity.

- Transition to Digital Payments: The transition from cash to digital payments is ongoing, with different countries and demographics moving at different paces.

- Impact of the Pandemic: The pandemic accelerated the shift from cash to digital wallets, especially among younger generations.

- Digital Trust Issues: There is significant distrust in digital payments due to concerns about privacy and government surveillance.

- CBDC and Anonymity: Central Bank Digital Currencies (CBDCs) aim to replicate cash's anonymity, but there are challenges in convincing the public of their privacy.

- Future of Digital Transactions: The future will likely see a mix of national currencies for physical transactions and cryptocurrencies for digital transactions, with ongoing debates about privacy and trust.

The full discussion follows ...

Question: What’s the future of cash and digital cash?

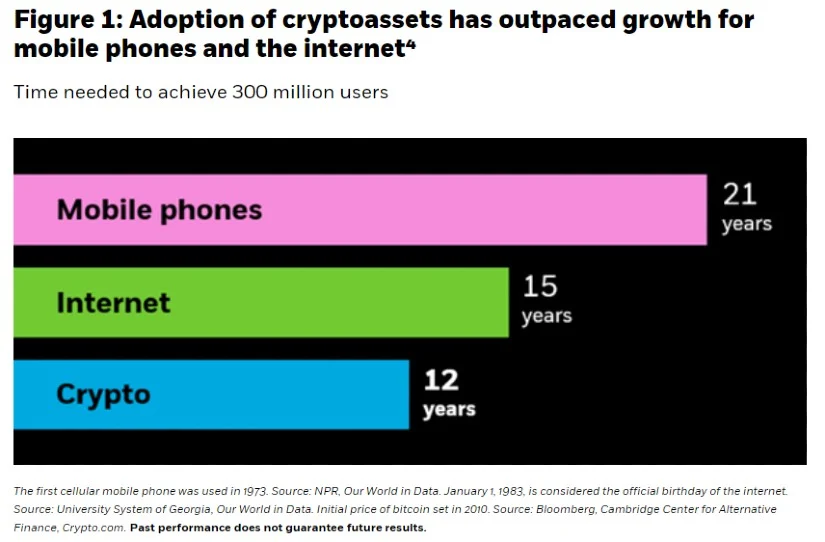

Chris Skinner: Let us start with being clear that we have a multi-tiered demographic. You’re going to have currencies that appeal to the technology community and those who are really capable of understanding cryptocurrency, of which it was a small number ten years ago. It’s now a much larger number. In fact, there was a study that came out the other day from Blackrock, that says that the use or the acceptance of cryptocurrency has been faster than the use and acceptance of mobile and internet technologies reaching 300 million users in just 12 years of crypto.

But when we say users, that’s actually not paying for things. That’s mainly people using it to invest and looking for speculative return, in my opinion. So that’s one community.

Then you have another community, which is your mother and father or someone just on the street, who has no technology understanding or just basically uses Wi-Fi, and who’s not interested in these speculative investments or, if they are, they find it difficult to find out how to use them. For them stable coins and government currencies that are digitally issued is going to be appealing.

Then you have a third community, who do not trust anything other than cash. You may say, well, who are those people? In my view, it’s those who want to deal direct with trust, without government involvement, and can make something happen immediately, such as paying for someone doing my gardening or paying my local scouts club and those sorts of things.

In fact, that’s quite funny because the UK tried to ban the use of cheques twelve years ago, and got a huge backlash. The main reason being is that there was no alternative to cash and cheque that is as easy to use and as seamless and frictionless. You may say, okay, PayPal using your bank’s digital app twelve years later is a good replacement, but that is not anonymous.

This is the critical point: it has to be anonymous. Cash is anonymous and is why it is trusted. What is the digital equivalent (there are a few, but I’m not going to tell you).

Question: You identify three groups, and I think that’s totally fair point that we have different demographics who have different behaviors, different cash habits or different currency habits. We have the first one that is open for technology. We have the second one, our mother and father generation who might have some scepticism about all this digital stuff. The last one, which you made up, are always just sceptical about anything that comes from a government. I think they are really difficult to change their habit in the future. That’s also why I think that cash will still stay in the future because, especially for this group, I think there is no other alternative. Meanwhile, for my mother and father generation, of course, they will fade out at some point in time. So, there will be a generation – those digital natives as we call them – who grew up with technologies, who are aware of technologies and how it works. This means there will be a transition into more and more digital, but still we have this sceptic group, the last one which you made up. For them, cash will still play a crucial role in the future. This is why we must focus on both physical cash but also on digital alternatives and make both cycles as resilient.

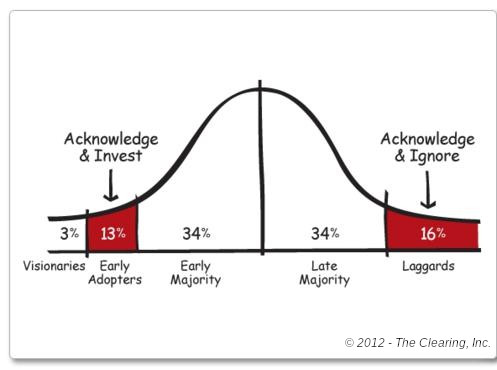

Chris Skinner: We’re in that classic cycle of leaders and laggards and the majority. It is that classic chart that goes round that way in the S curve.

And if we’re talking crypto, then we’ve got a lot of people who were early in the game who were innovators. If we’re talking cash, most of them are laggards at the back end of the curve, who are still believing that that’s the best way to pay. And in the middle, it’s not a demographic actually, it’s a complete mixture of those who are using digital banking and FinTech apps, who enjoy that convenience. The cash piece, I guess the core of it. We could do a massive survey, but we’ll just do it between the three of us. When was the last time you felt you had to use a paper cash note?

Question: I try to use as a little cash as possible, and only pay with cards. The last time I paid with cash was for an event that didn’t accept card payments. It’s a matter of geography. That event was in Germany.

Chris Skinner: Exactly. Everyone and every country is moving at a different pace.

I was at the Euro football finals last year in Berlin and Munich, and I went to one place – a museum – and they said, oh, you can only come in if you pay with cash, and so I didn’t go into the museum because I didn’t have any cash. I only pay by card or digital wallet these days. I don’t carry currency.

This is indicative of where we’ve got to, which is a transition from cash to contactless and card to digital wallet to whatever is the next thing, which is tokenisation. We can now just tokenise value. Whether it’s digital or physical assets, it’s just tokenized on a smart contract or distributed ledger technology.

Equally, the pandemic changed behaviours. It changed most people’s behaviour to stop using cash, because it transmits bacteria and you don’t need it. I was using card a lot of the time, but card can also transmit bacteria and it’s not needed. This is why many of us have ended up using digital wallets more. It’s contactless and on the phone, so you don’t have to carry anything other than the phone, which is always with you. Leave the house or office without your phone and you feel you’ve left your soul.

So there’s a general consumer movement, particularly among Gen Z and millennials, but also more likely amongst boomers, which is to move from physical to digital services and wallets. That’s the reason why there is a fight over who owns the digital wallet because, if you own the digital wallet, you own the customer. That’s why Apple’s made a big play here with ApplePay and also with privacy, which is one of the things that Apple’s championing as part of their proposition.

We are in interesting times and it’s a transition that’s happened. It’s taken thirty years and, in the next thirty years, it becomes a totally different proposition because you don’t need a wallet, you don’t need cash, you don’t need a card, you don’t need anything. You just need to blink or tap or swipe, which is almost where we are at already.

Question: This reminds me of Sweden, as an example, going very fast into cashless then, suddenly, it stopped at around 8% of cash payments and started to push back. Last year, the government even had to issue some legislation that banks should still provide the infrastructure for cash to protect this. Do you think there will be an equilibrium between digital payments and cash payments or it’s a process of digitalisation and cashless that will go on and on.

Chris Skinner: Well, there’s two or three things in what you just said, particularly Sweden, because Sweden is a great example in Europe of how to look at the move towards the digital age. They try and be at the forefront of everything digital.

Sweden was the first European nation to start using cash, and now they’re trying to be the first European nation using digital cash.

One of the key things as you just referenced is that, although they’ve pushed this very hard in the last thirty years, Sweden still hasn’t got rid of cash and the reason is that not everyone wants to get rid of cash.

A good example is in their neighbouring country: Denmark. Just look at Christiania in Denmark, who want to retain freedom from government and governance. Cash gives you that freedom. So unless you can give me an exact equivalent of cash digitally, I’m not going to change my behaviour. And there are digital equivalents of cash, particularly in the crypto world, just that most are associated with criminal activity, whether truth or not but, going back to what I said before, not everyone is a technologist or geek or nerd, and so they haven’t quite got the message.

The second thing is I found it very interesting in Sweden in that we were doing work in Stockholm, with one of the startup centres there, and the guy who runs the centre showed me that he had a chip in his hand, which is a government issued chip for NFC payments. This meant that he could go anywhere in Sweden on the transport network and didn’t need anything other than to just put his hand on the terminal. The thing is that he then made the point that, although this was issued by the transport and government network, only a few thousand Swedish had signed up for the program because most people were worried. They were worried that the government was going to track and trace where they were and what they were doing. This was a passive NFC chip, with no communications. Even so, people didn’t trust it.

This is the fundamental which is identity and how we live.

In fact, it’s the theme of my next book, which is digital trust. How do you know you are you when it comes to digital exchange?

I always remember presenting to an Eastern European audience twenty years ago, and talked about digital identity and having everything on the network. The idea that the system could recognise that you are you through biometrics, voice and face, when a someone from the audience said, oh, we used to have identity cards and we don’t like them very much.

https://www.youtube.com/shorts/povWJLiJNJ0

This is the problem in Sweden and in every country, and it’s the reason why cash is still predominant even though it may be only 8%. The core challenge is that I don’t want you or the government or state to know what I’m doing. It is why cryptocurrencies have been created.

Question: Absolutely. That’s one of the advantages of CBDC, retail CBDC, where the level of anonymity, technically it can be anonymous. Of course, the government would not agree,

Chris Skinner: The problem with retail CBDC is that the banks don’t want the central banks dealing direct with the public as that eradicates their purpose. I mean the only reason for CBDC is because governments are worried about cryptocurrencies, which are global and have no borders and then, when you look at CBDC, you have an argument of a retail versus wholesale distribution of the currency.

Banks would argue that has to be through the banking system, otherwise their role is diminished or eradicated. Governments might believe it’s more relevant for them to issue directly to consumers and to the markets because that creates volume and growth. So, we’re going through a massive transition.

The bottom line is that most digital currencies will be transacted globally through the network of the people based on the most popular mechanism available, which will be some form of cryptocurrency. I don’t know which one yet because it changes every day. Ripple, Bitcoin, Ethereum, Cardano, Polygon, Dogecoin or whatever.

National currencies will be the physical way in which you transact so national currencies for physical transactions, cryptocurrencies for digital transactions,

Libertarian versus state. That’s the big debate.

Question: You mentioned that cash gives you freedom and, as long as a digital alternative doesn’t give you the same freedom, you’re not willing to use it. This is exactly what CBDC initiatives worldwide are trying to do – to mirror cash into the digital world – like having a digital twin of cash. The problem is that you have to convince people that it’s actually the same as cash. For example, if you use the digital euro and the central bank says it’s going to be private, does that really mean that they won’t track your payment history? How do you prove it to people that there’s no data processing in the background?

Chris Skinner: This is the key. Going back to digital trust, you have these layers of trust and the easiest layer of trust is a physical transaction that’s immediate. You do the transaction, walk away and everything is clear. Now, the government can say you can do that transaction digitally just as easily with the same level of trust, but then you’ve added two third parties to the mix of the exchange: the government and the financial intermediary.

This creates distrust.

The reason why this creates distrust is because you have created further brokerage between the immediate exchange which cash gives you physically by adding third party interventions.

It is these layers of trust that I’m exploring in my next book, which is focused upon how to create the same level of trust in a digital exchange that you have in that physical exchange. How we create it and convince people to believe in it. That is the next level and that’s where the biggest issue lies. How do you make people comfortable about making a digital exchange of value where they trust the person they are doing business with, but cannot be tracked and traced? This is a fundamental question and the biggest barrier.

The biggest barrier on top of that is how do you create digital trust when hoards of the criminal fraternity and the scammers are involved in these loops. So many disturbers who aim to buck the system and create huge amounts of fraud and loss. So many layers here of trust and distrust and crime and honest exchange. This is not new. We’ve had this ever since mankind became civilised, so to speak, although we’re still working on that one.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...