Way back in the 1990s, we all talked about object-oriented architectures and modular computing. In the 2000s, I called it Banking-as-a-Service, BaaS, and started presenting the idea around the world.

The difference between the 1990s and 2000s was cloud and mobile smartphones. This change was the tipping point from fragmented systems to open platforms, and the move to apps and APIs.

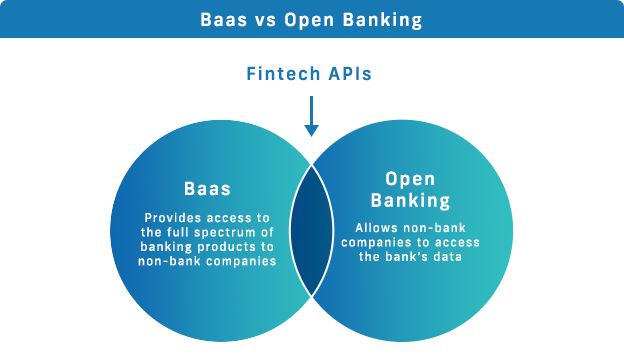

Twenty years later, we take BaaS for granted and talk about ecosystems and open banking but, tracing its roots, it goes way, way back to the idea of breaking down banking processes and automating them with plug-and-play software. This allows us to take all the pieces and ingredients of a financial process and recreate it in minutes. Taking that one step further, and this was my idea of the 2000s, you could take lots and lots of start-up providers of financial services and create your own bank. Here’s that slide (2009):

I guess the biggest change is that almost every single process within a bank now has a third-party API that you can quickly plug into the ecosystem to build a bank. This is why we have so many fintech firms succeeding by specialising in part of the process of finance, rather than the whole construction of a bank.

But what does this mean to banking in the future? Well, the biggest question has to be around risk and regulation. How are the many parts of the financial system structured, regulated and who will be accountable if it all goes wrong?

These are the questions always asked by yours truly when placing my money somewhere. Is it guaranteed and covered by a financial compensation scheme? As far as I’m concerned, it is then the company – the bank – who are accountable for my money and guaranteeing its safety.

The issue this raises if the bank brings in a third party to run part of their processes, they are no longer in control and, because they are accountable for all risk and regulation, they therefore don’t want to bring in their parties to their processes.

However, with more micro regulations to provide emoney providers and more, the market for money is becoming far more granular. By way of example, there are almost a dozen in Estonia, and they seem to be growing by the day:

- Virtual Currency Exchange license and e-wallet license

- Financial Institution license

- E-money Institution license

- Payment Institution license

- Investment Firm license

- Fund Manager license

- Credit intermediary license

- Credit institution license

- Insurance broker license

- Insurance company license

- Travel Undertaking license

These licensing systems from regulators will get more and more regulator, and the point I made back in the 2000s is that no customer wants to do the due diligence of 1,000 start-ups to see if they are licensed and regulated. I want my bank to do that.

In other words the role of a bank these days is to curate the fintech ecosystem and bring in trusted third parties who are regulated and have been vetted by the bank to be part of their platform. This point is nothing new – I was saying it almost twenty years ago – but it very hard for many banks to accept as they still believe they have to do everything internally to control the risk exposures.

I know this is changing, but it is also clear that many bank leaders and internal cultures are still pushing back against such a structure. If this is true, it is a bank that won’t be around for much longer as there are plenty of new banks that are doing this really well. Just take a look at 11fs Foundry, Starling Bank’s Engine or Solaris Bank’s APIs. There are many other BaaS providers out there – banks that offer API services to automate processes through plug-and-play software, including Clear.Bank, Treezor, Intergiro, Finastra and more.

The BaaS market has developed and evolved over three decades into a mature market that traditional banks need to embrace. It’s not an ecosystem. It’s an open system.

Source: SEPA-Cyber Technologies

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...