OK, OK, OK, I promise to stop posting predictions and trends and blah, blah, blah, but this one has an interesting provenance and history. Last year, one of my most read blog entries was this one: The top ten trends in banking innovation (February 2016). This was a summary of the top trends in banking innovation, and was based upon the Accenture/EFMA 2015 research paper, which is published annually. Therefore, to finish off the trends tracking, here’s their new report.

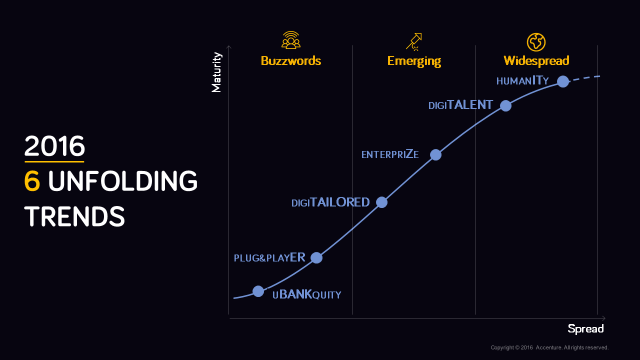

6 unfolding innovation trends, 1 booming interaction model

Accenture and EFMA recently held in Barcelona the closing ceremony of the 2016 Distribution & Marketing Innovation Awards, their joint initiative aimed at identifying and appraising the most innovative projects in Retail Banking at global level.

When the program was launched back in 2013, it was no more than the dream of a group of banking innovation lovers. But in just 4 years it grew enormously, becoming the place to be for banks looking for showcasing, networking and learning together with the industry benchmarks.

Indeed, the 2016 edition saw more than 200 banking players from 61 countries worldwide submitting over 460 innovative projects across 10 different categories, ranging from Customer Experience to Big Data, Analytics & Artificial Intelligence.

The deep analysis of their inspiring contributions, together with the ongoing activities led by Accenture through its Innovation Series observatory on banking innovations, helped unveil 6 innovation trends that are shaping the evolution of Retail Banking.

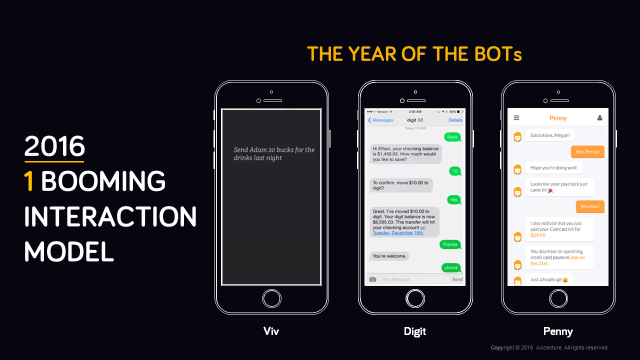

Of course they are at different levels of maturity and spread. Some of them are still buzzwords, others seem to have reached their peak, while a few of them are now very well embedded into banks’ innovation DNA. But regardless of their stage, they all seem somehow influenced by a new, disruptive interaction model. In fact, 2016 saw the merger of Artificial Intelligence and Conversational Interfaces, up to the point that made many observers talk about “the year of the bots”. And, as we’ll see, the successors of Siri are now pervading banking as well.

FIGURE 1 - 2016 INNOVATION TRENDS

FIGURE 2 - 2016 BOOMING INTERACTION MODEL

Let’s have a closer look at the trends behind this year’s huge innovation efforts by the global banking community

Trend #1

The first trend spotted by Accenture, “uBANKquity”, is about banking institutions letting customers bank outside traditional boundaries, directly on third party properties or via smart, hyper connected devices.

Capital One Skill for Amazon Alexa is a powerful example. As part of its commitment to shape cutting-edge, customer-centric services, the bank recently entered into an agreement with Amazon to launch the first, impactful example of IoT in Banking. Thanks to this initiative, the bank now allows its customers to track their spending, check account balance and pay their bills just by interacting with Alexa, a hands-free speaker that plays music, provides information such as sport scores and does many other things via simple voice commands.

Another iconic example comes from Spain, where Banco Sabadell announced the launch of CUBs, an electronic device with digital banking features that help customers reach financial goals and manage their money, while improving kids’ financial education.

But it’s not just about IoT. uBANKquity also appraises the terrific attempt by banks to be right in the digital places where their customers are. And this year a turning point has been observed. In the recent past we’ve been used to see banks introducing non-financial services within their digital properties to attract customers and increase contact frequency. Nowadays, we see institutions building a strategic, digital presence where customers and prospects fulfill their everyday needs, such as e-Commerce websites or online travel booking tools. And it’s getting quite common to find offerings of financial solutions, such as consumer loans or insurance products, right at the check-out of Apple or Expedia websites. This move lets banks expand their distribution network and boost interaction opportunities with low effort, being able to offer time-relevant solutions to their consumers.

Trend #2

The second trend, “plug&playER”, is shaped by those players that inject capabilities and applications provided by third parties - mainly Fintech - to speed up a wide range of activities and operations, from bank foundation to IT architecture set-up, up to the expansion of digital service portfolio with reasonable set-up costs.

And Banco Original, Most Disruptive Innovation of the fourth edition of EFMA-Accenture Innovation Awards, is such a compelling proof. The Brazilian mobile-only bank was created with an Open Banking philosophy, thanks to a partnership with a Fintech accelerator program and a dedicated API platform that let the bank avoid long-lasting, in-house IT development and enter the market in just a few months with a disruptive value proposition. This is a strategy that perfectly mirrors the point of view of Mr. Guga Stocco, the bank’s Head of Strategy and Innovation, that recently stated “If you have a team who’s going to build some products, their size should be no more than the number of people who you can feed with two pizzas. [...] If you need more than two pizzas, it means that the team is too big and you will lose the momentum”.

Banco Original is a trailblazing case, but not the only one. N26, the millennials-dedicated digital platform with European scale, is another interesting example: it was created from scratch by putting together third party providers to introduce very quickly systems and services, such as KYC, P2P payments, and Robo Advisor solutions.

But it’s not just a game for digital attackers trying to emerge and prevail through an agile IT architecture. In fact, the banking landscape now sees many incumbents partnering with Fintech to widen their service portfolio, such as ING, that chose Kabbage to expand its lending capabilities to SMEs.

Trend #3

Climbing the innovation curve, we find the first digital-enabled trend beyond the “buzzword stage”: “digiTAILORED”. As its name suggests, the trend embraces all those players that exploit the digital lever to shape a tailored value proposition for specific customer niches.

As the dear old long-tail theory by Chris Anderson suggests, digital today enables organizations to serve customer niches, such as demographic or mindset-based clusters, in a cost-effective way, something that used to be considered impossible from any company with a physical-first distribution model. And this is exactly what many forward-looking digital attackers and a few incumbent players are doing. Standard Bank and Santander, for example, are seizing the digital opportunity to shape touchpoints, offering and relationship model around specific needs of specific customer niches, thus boosting customer acquisition and share of wallet with no cost-to-serve shocks.

Standard Bank, one of the finalists for the Most Disruptive Innovation Award, recently announced the launch of Shyft, to meet the underserved needs of the community of frequent international travelers. Shyft is a mobile-only solution that lets customers manage all ForEX operations, make P2P payments to anyone across the world and pay in the local currency avoiding huge conversion fees. This kind of service could be a turning point for these citizens of the world, that are always on-the-go monitoring exchange rates and waiting at the airport money exchange facilities. Without forgetting the huge fees they are charged when spending or managing money abroad.

Another incumbent player moving in this space is Santander. The Bank is targeting kids under-18 and their parents with the Santander 1|2|3 Mini program. The initiative brings together a kids-dedicated offering and a gamification-based tablet and mobile app to ease money management and increase kids’ financial literacy, while giving parents the control and the security they need.

Another interesting, noteworthy example comes from UK, where the digital attacker Monese introduced expats-dedicated onboarding processes and transactional services. This challenger bank aims to target the expat community, solving the trickiest points for expatriates looking for establishing a banking relationship: the account opening. Hard to believe, this process can be very difficult with banks always requiring something expats can’t get soon: a residency proof. Thanks to Monese, all European Economic Area residents can now open an account immediately, regardless of their citizenship or financial history. And this is possible thanks to a wide set of technologies that Monese has adopted, such as its system able to check multiple data sources from all over Europe for address validation.

Trend #4

The forth trend, “enterpriZe”, is about banks realizing that business customers deserve more. As a matter of fact, we are witnessing a restless effort to provide businesses with Value Added Services able to support them throughout the entire business lifecycle, even before and beyond cash management needs. We see banks expanding their core offerings with digital-native, non-financial services able to meet actual customer needs while increasing their stickiness and share-of-wallet in a cost-effective way.

KBC Securities, for example, recently launched Match’it, a forum-like digital platform that supports small businesses in their M&A operations, from counterpart scouting to due diligence and deal closing, through KBC network and the expertise of the bank’s advisors.

But the array of value added services goes beyond complex corporate finance operations, ranging from services to ease the business set-up to platforms supporting businesses looking for entering new, foreign markets. ANZ, for example, offers a wide set of solutions to help entrepreneurs start their business. In its Small Business Hub, the Bank offers customers and prospects tools to build an effective business plan, run SWOT analysis or calculate break even point. But for entrepreneurs looking for further support, the bank offers even more through its Business Ready program powered by Honcho, a Sidney-based company. Business Ready helps companies move from idea to practice and run their business better, offering services such as business name registration, logo design and webpage building to market their value proposition.

Trend #5

Moving to those trends that are widespread within the industry, “digiTALENT” is the next stop of this 1-year-long journey. We are in the space where banks embrace innovative technologies to provide an intelligent, always-on support to their frontline people. After introducing cutting-edge digital services and self-service capabilities, human-driven contacts got rare and much more important at the same time. When meetings run low, pitfalls in managing every single interaction are no longer an option. This is why financial institutions are introducing tools to empower branch employees and contact center reps with additional intelligence to excel in one-to-one interactions and provide an excellent customer experience.

The examples in this space are numerous. Among them, the initiative launched CaixaBank, global innovator of the 2016 Innovation Awards, is definitely one of the most noteworthy. The bank implemented a virtual assistant in Foreign Trade that lets about 28,000 employees ask questions in natural language to the financial terminal and quickly access information and documentation about letters of credit.

On the other hand, Swedbank introduced a similar solution to help its customer service reps easily manage customer queries, thus improving workload management and, as a consequence, satisfaction levels.

But Artificial Intelligence is not the only solution to help frontline employees in managing meaningful conversations with their customers. Emirates NBD, for example, recently launched a tablet app integrated with CRM tools and the branch queue system, letting branch staff spot and fast-track customers that are waiting in line. The app is also empowered with an innovative feature able to calculate the time saved by each customer, a valuable information that the bank encourages to share at the end of each transaction to create a WOW experience.

Trend #6

Last but not least, we have “humanITy”. This is the space where the concept of 2016 as the “year of the bots” is mirrored the most.

On one hand, Artificial Intelligence technologies are able to simplify the User Experience and boost self-service channels adoption, as the DBS story suggests. The South Asian banking giant launched in June digibank, the brand-new mobile bank staffed by Kasisto chatbot, a technology able to anticipate and answer thousands of customer questions (both text and speech) and perform banking transactions in real-time. A technology that revolutionizes the way customers interact with the bank and manage their finances, allowing them to “Live more, bank less”, as DBS’ CEO recently stated.

On the other hand, Artificial Intelligence allows banks to provide human-like advisory services through their digital properties, thus opening the advisory doors to customers that are traditionally not eligible for this kind of services. Among many other players globally, BBVA Compass for example is leveraging FutureAdvisor’s Artificial Intelligence to convey wealth management advisory services also to upper mass customers.

Closing remarks

As for any trend analysis, the year after is always a good litmus paper to get confirmations, approvals and new sparks. Among the answers we look forward to receiving there is the role bots and conversational interfaces are going to play. Time for apps to disappear seems far today and probably a more hybrid approach will prevail, at least in the short/ medium term. But the speed of bots development and enhancement is terrific and we will probably observe new shakes in the interaction model field. Other fascinating fields of additional investigation are related to IoT, that is no longer an insurance-only battlefield and API. Open Banking is a now a solid option also for incumbents and it will be great to see how deeply they will go for it and how many “bank as a platform” models will see in the market in the next few months.

This article was written by the Accenture Research leads on this project: Ambrogio Terrizzano, Antonio Coppolecchia and Carlotta Bernabei.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...