I haven’t blogged much about Europe or other things other than Fintech lately. I guess because Fintech is taking up so much of my time and discussions, but the Greek crisis has not gone unnoticed in the news headlines or in my thoughts.

For some, the Greek crisis has been a joke …

… but for Greeks it is no joke. It’s a deeply harming situation that has created poverty for the affluent masses and suicide for some: “tough financial austerity measures in Greece have led to a 35% jump in suicide rates in a little less than 2 years, new research shows.”

This is no joke, but what is at the heart of the matter is the Eurozone.

The Eurozone purely hangs together thanks to Germany’s strong hand, and many commentators have been pointing the finger at Germany and saying it is their strong economy that is ruining others.

Bloomberg, 17th July 2015: “Were Greece to leave, possibly followed by Portugal and Italy in the subsequent years, the countries' new currencies would fall sharply in value. This would leave them unable to pay debts in euros, triggering cascading defaults. Although the currency depreciation would eventually make them more competitive, the economic pain would be prolonged and would inevitably extend beyond their borders. If, however, Germany left the euro area -- as influential people including Citadel founder Kenneth Griffin, University of Chicago economist Anil Kashyap and the investor George Soros have suggested -- there really would be no losers.”

The Telegraph, 21st July 2015: “Influential figures including Ben Bernanke have called on Germany pull its weight to end the Eurozone's dysfunction. The only alternative is a German exit from the euro”

The Financial Times, 13th July 2015: “Preventing Grexit is France’s chance to stop a German euro.”

Perhaps the situation is best summed up by Foreign Policy magazine back in February:

“Last year, Germany racked up a record trade surplus of 217 billion euros ($246 billion), second only to China in global export dominance. To some, this made Germany a bright spot in an otherwise anemic Eurozone economy — a “growth driver,” as the German finance minister, Wolfgang Schäuble, puts it. In fact, Germany’s chronic trade surpluses lie at the heart of Europe’s problems; far from boosting the global economy, they are dragging it down. The best way to end this perverse situation is for Germany to leave the Eurozone.”

So could Germany leave the Eurozone and, more importantly, what would it mean if they did?

This is not a new idea, and has been floated by many thinkers for some time. Perhaps the most important contribution to the recent debate on the matter came from George Soros in 2012. In an interview with Spiegel Online in June 2012, this exchange sums up why Greece has some rightly pushback on the German plan:

SPIEGEL ONLINE: Germans remember the birth of the euro very differently. They felt they had to give up the deutschmark in order to get other European Union nations to agree to German reunification.

Soros: True. The integration of Europe was very much led by a Germany that was always willing to pay a little bit extra to reach a compromise that everybody accepted, because Germany was so eager to get European support for reunification. That was called the "farsighted vision," which created the European Union.

SPIEGEL ONLINE: Do we need a similar vision today?

Soros: I want to draw the parallel between what is happening with the euro zone right now, and what happened after World War II, when the Bretton Woods system of monetary management was created to govern the global economy. Then, America became the center of this system, and the dollar became the dominant global currency. It was a free world dominated by America. But America earned that position by providing huge funds for the reconstruction of Europe through the Marshall Plan. America became a benevolent imperial power, which greatly benefited America.

SPIEGEL ONLINE: How can that situation be compared to the one in which we find ourselves today?

Soros: Germany is in a similar position today, but it is not willing to engage in anything like the Marshall Plan. It is opposed to any transfer union for the rest of Europe.

SPIEGEL ONLINE: The Marshall Plan, though significant, amounted to just a small share of the US gross domestic product. The potential payouts related to a euro rescue program, on the other hand, might be more than Germany can handle.

Soros: Nonsense. The more comprehensive and convincing a debt reduction program is, the less likely it is to fail. And remember, just as Germany is grateful to America for the Marshall Plan, Italy would be grateful to Germany for helping it lower its refinancing costs. If it did that, Germany could set the conditions. And Italy would be happy to meet those conditions, because it would benefit from it. Not to recognize this opportunity is a tragic, historical mistake by the Germans.

However, to portray a Gerxit rather the a Grexit is not a balanced discussion unless you include the alternate view, and there always is one. Professors Iain Begg and John Ryan of the London School of Economics call the idea of a German exit a disaster:

"After European Union membership, I think the construction of the euro is one of the greatest achievements that Germany has been able to achieve post-war. From a political point of view, there's been a lot of capital put into the project. Going out of the euro would maybe send a bad message for the sustainability of the EU as well. And Germany leaving the euro would just send an absolutely crashing message, and it's not conceivable to think that the Eurozone could really survive after that."

Either way, the final solution to Greece’s unsustainable debt problem is still unworkable. From this morning’s Sydney Morning Herald, Greece's banks are dying, and fast:

“Greece's purchasing managers index, which measures manufacturing activity, just collapsed from a sickly 46.9 to a deathly 30.2. Anything less than 50 means that the manufacturing sector is shrinking.

That, in turn, means that Greek businesses that should have been able to pay back what they owed won't be able to do so. And so the Greek banks that lent them money - which, at the time, was a perfectly reasonable thing to do - are in line for more loss. How much more? Well, enough that their stocks have fallen by the maximum 30 per cent almost every day since the country's markets reopened. Add it all up, and Greece's four biggest banks have plunged between 80 and 90 per cent since last October. At this rate, it won't be long until they need the €10 billion to €25 billion bailout that Greece's creditors think it will take to recapitalise them.”

So maybe Germany will have to leave the Eurozone to keep the zone sustainable, or maybe Greece will leave by default – further default – and its economy will be in ruins for years to come.

Cartoon sourced from Daily Forex

A map of the Eurozone, based upon credit ratings today by Fitch:

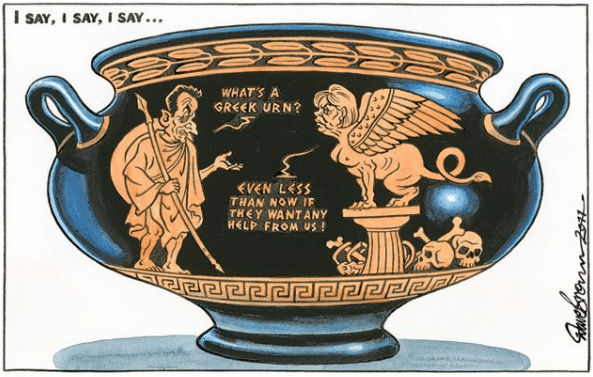

* in case you didn’t get the first cartoon's joke, here’s an explanation via Jeffrey Hill’s the English Blog

This cartoon by Dave Brown from The Independent is based on an old music hall joke: "What's a Greek urn (i.e., earn)?" "About 30 shillings a week" (or some other sum of money). Music hall jokes traditionally begin with one half of a double act asking a question beginning with "I say, I say, I say", and the other half delivering the punchline.

The joke depends on the fact that 'urn' and 'earn' are homophones, and "What's" could be a contraction of "What is" or "What does". So the question is understood as "What does a Greek earn?" rather than "What is a Greek urn?" (an urn is decorated vase).

The cartoon shows the then French President Nicolas Sarkozy (this was June 2011) asking the question, and German Chancellor Angela Merkel (portrayed as a merciless and treacherous Sphinx) replying "Even less than now if they want any help from us!"

EXPLANATION

The cartoon relates to the Greek debt crisis. Angela Merkel has reluctantly agreed to another bail-out of the debt-laden Greek economy, but in return she will be expecting the Greeks to tighten their belts even further.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...