So Facebook announced clarification of plans to rollout Facebook Pay, an easy way to pay friends through Facebook using your debit card.

They had considered credit cards, but want to avoid fraud and risk and felt the debit card is the way to go. Initially US-based, the service will gradually be released worldwide. Here are the key points from Facebook’s own release:

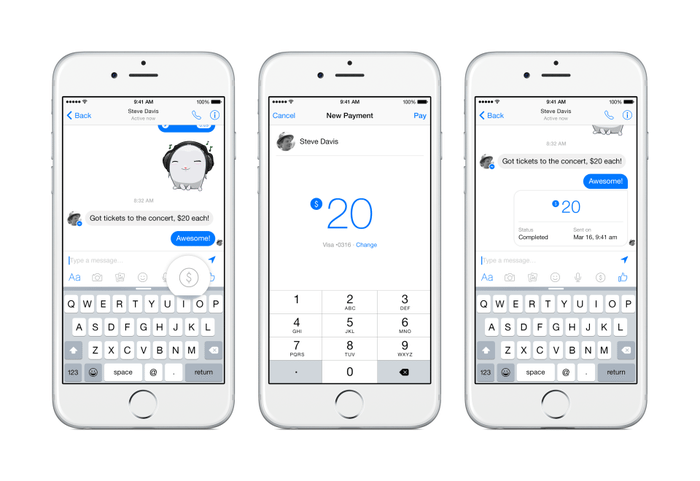

Today we’re adding a new feature in Messenger that gives people a more convenient and secure way to send or receive money between friends. This feature will be rolling out over the coming months in the US.

It’s easy and free.

To send money:

- Start a message with a friend

- Tap the $ icon and enter the amount you want to send

- Tap Pay in the top right and add your debit card to send money

To receive money:

- Open the conversation from your friend

- Tap Add Card in the message and add your debit card to accept money for the first time

The money you send is transferred right away. It may take one to three business days to make the money available to you depending on your bank, just as it does with other deposits.

Secure Network

A dependable and trusted payments processor for game players and advertisers since 2007, Facebook processes more than one million transactions daily on the site and also handles all the payments processed on Messenger.

Incorporating security best practices into our payments business has always been a top priority. We use secure systems that encrypt the connection between you and Facebook as well as your card information when you ask us to store it for you. We use layers of software and hardware protection that meet the highest industry standards. These payment systems are kept in a secured environment that is separate from other parts of the Facebook network and that receive additional monitoring and control. A team of anti-fraud specialists monitor for suspicious purchase activity to help keep accounts safe.

The first time you send or receive money in Messenger, you’ll need to add a Visa or MasterCard debit card issued by a US bank to your account. Once you add a debit card, you can create a PIN to provide additional security the next time you send money. On iOS devices you can also enable Touch ID. As always, you can add another layer of authentication to your account at any time.

The new payments feature is rolling out in the coming months in the US across Android, iOS, and desktop.

I did silently chuckle that this announcement came out on Tuesday following Monday’s announcement of Facebook’s rules related to nudity. After all, a social network doesn’t want to be plagued with people using their debit cards to buy and sell sexual favours, do they? (you’ve got bitcoin for that)

Anyways, is Facebook Pay any good? Techcrunch gives a good analysis of the technicalities of the service, and note that it’s been built in spite of convenient alternatives like Stripe, Square and PayPal, Facebook’s partner of choice for payments since 2008. In response to the question of the split, PayPal said:

We have had a great relationship with Facebook since 2008 and currently work closely together to deliver easy payments on a global scale for its games and ads businesses. PayPal has always taken a partnership approach to payments and we will continue to work with Facebook and many other companies on new payments experiences that make it easier for people to send and receive money on both the PayPal and Braintree platforms.

I bet.

What intrigues me with Apple Pay and Facebook Pay is a different theme however, as we now have two big heavyweights in the world of technology weighing in on payments. Their aim: make it easy, cheap and convenient to pay whilst engaged in entertainments, sharing and fun.

Removing the friction of payments. Isn’t that what we’ve been saying banks should do?

Regardless, the good news is that Apple and Facebook have deigned to allow banks to still play in the game of money online. The bad news is that banks are now wrapped in a stranglehold by these major players, and Google and Amazon are still to play (not forgetting Yandex, Alibaba and co).

The evidence of what this means is that banks are going to be squeezed on margin. We’ve already seen this with Apple forcing lower fees per transaction from their bank wallet players, giving Apple a slice of margin off the top that equates to billions when you multiply 800+ million iTunes accounts making an average $3.2 in transactions per month (reference Asymco, 2013).

Facebook’s model will follow the same approach over time, I’m sure, as banks don’t want to lose the opportunity and threat of being included or excluded from these heavyweight players networks. But it’s not the banks I feel sorry for, but Visa and MasterCard. Right now, the card companies have been very adept at pushing the envelope of innovation. They’ve been at the heart of contactless rollout, NFC and pushing the mobile wallet wars. But what happens if an Apple or Facebook came out tomorrow and said that they’re now going to be transaction rails to your bank? Visa and MasterCard (and the rest) wouldn’t stand a chance.

I’m not saying they will do this, as it would involve too much negotiation with banks and such like of course, but there are those who think they will and those who think they won’t.

To be honest, it may not be in their interest to do anything but let’s just say that one day they introduce a view that all of your payments will be taken monthly from your bank account, or any other preferred source, for a charge of $1. In so doing, you get a 5% reduction in all your purchase costs. The reduction is because there are no fees being taken by the card companies and retailers and banks have agreed a good deal with Apple to be in the loop.

Just sayin’ …

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...