The World Payments Report (WPR) has just

come out. It is the 8th

report produced by EFMA, in partnership with Cap Gemini and the Royal Bank of

Scotland (ABN AMRO previously), and provides a good analysis of global payments

movements in the same way as we do with our European Payments Report, produced

in partnership with Logica and the EBA (if you want a copy of the European report, email me).

The World Payments Report is in three sections. The first looks at non-cash trends in the move

towards epayments and away from cheques; the second section studies the

challenges the industry faces in terms of regulations; and the third looks at

customer-centric innovations across the industry and the future.

With a report full of fact and data, I felt

that it’s not worth just squirting out a quick summary of the whole thing, so here’s

a breakdown in four blog entries of each section of the report, with one

specifically on the trends related to SEPA and Europe as that’s my specific

domain of expertise and focus.

Section

One: The World Non-Cash Markets and Trends

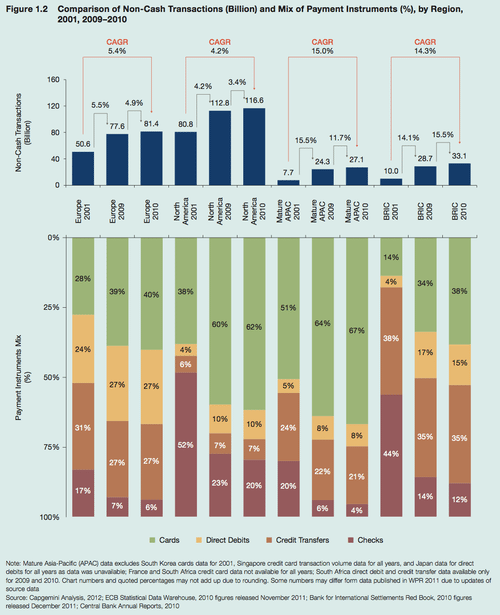

The global volume of non-cash payments

continues to show healthy growth, with the largest gain in volumes occurring in

developing markets.

Volumes grew by 7.1% to reach $283 billion in 2010, the most

recent year for which official final data is available for all regions.

Volumes

jumped 16.9% in developing markets, boosted by an increase of more than 30% in

both Russia and China. That growth far outpaced the modest increase in volumes

in developed markets, which were still suffering the effects of the financial

and economic crisis.

Even in developed markets, though, the growth in non-cash

payments volumes, at 4.9%, outpaced the rate of growth in gross domestic

product (GDP), and developed markets still accounted for about 80% of all

non-cash payments transactions globally.

Cards (debit cards and credit cards) are

still the biggest driver of non-cash payments volumes globally.

Cards accounted

for 55.8% of all non-cash payments in 2010, up from 53.4% in 2009 and 35.3% in

2001. Debit cards alone accounted for more than one in three of all payments,

partly as the use of cards for smaller-ticket transactions becomes more

widespread.

The aggregate use of checks continued to decline (down 6.7% in

2010), while the outright volume of credit transfers and direct debit

transactions continued to increase in 2010, though the relative usage of these

instruments is gradually declining compared to cards.

Global payments volumes are expected to

have reached $306 billion in 2011.

When global data are finalized for 2011, it

is expected to show the growth rate among developed economies rising only

slightly, by 5.6%, but the increase in developing economies is expected to be a

more robust 18.4%.

As a result, the share of payments volumes from developed

markets will have slipped again, to 77.7% in 2011 from 79.5% in 2010.

Electronic and mobile payments maintain

their rapid growth trajectory. Industry estimates show the number of online

payments for e-commerce activities (e-payments) is forecast to reach $31.4

billion in 2013, after growing by a sustained 20.0% a year in 2009-13.

Analysts

believe the number of payments using mobile devices (m-payments) could grow

even faster, by 52.7% a year to reach 17 billion in 2013. (This is faster even

than the rates being forecast just a year ago.)

Widespread innovation in

customer-focused m-payments solutions, especially by non-banks, is rising to

meet the growing demand.

With these markets growing so rapidly, there is a

mounting need for central banks to make sure reliable market data is being

collected and monitored with the same rigor for emerging payment channels as

for legacy instruments.

You can order a copy of the full report from EFMA, and the summary of each section is below:

- Part One, the Non-Cash Trends

- Part Two, the Regulatory Trends

- Part Three: SEPA

- Part Four: Innovation

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...