Last week, I blogged about innovations in payments from a consumer's perspective, and followed it up yesterday with an ancillary note.

In this second part, I thought I would take a closer look at what is innovatory in the corporate world of payments.

Many of us would immediately start talking about e-invoicing, supply chains and working capital. Sure, there is some innovation in those areas but the picture is bigger than this.

First, a little clarity of definitions, as per my lingo.

Commercial payments are the domain of the large transaction banks and their multinational and global clients. These are the mega corporations of the world we refer to affectionately as corporates.

It is not exclusively owned by these banks, as there are many national companies with domestic banks providing commercial banking very nicely thank you ... it's just that my mind wanders off into global processors with global clients when I think about commercial payments.

This is because there is a big change taking place here.

Until recently, these corporates had been fairly undemanding of their banks.

They were happy to have the odd lunch with their banker, who would fine dine and ego-boost them for an hour or two every month.

Taking their treasury operations, charging solid fees for transactions and generally making a good mint out of cross-border payments was food and drink to the banker.

This is where the money was to be made without stretching too far or too hard.

In particular, get the corporate to do their dealings through the bank via a proprietary link and you had ‘em for life.

After all, once the corporates general ledgers were hard wired to the bank’s systems, it was all but suicide for the corporate engine to switch to anyone else. This was especially true as the savings made just would not be worth the effort involved. A few cents here and a few pence there, per transaction, goes hardly unnoticed in the global wheels of commerce.

That was until standards arrived.

Standards.

The bug-bear of some, the bane of many and the blessing for the few.

The few who can work out how to leverage scale and exploit standards for volume savings.

This is what SWIFT do well – exploit standards for volume savings – but, until recently, SWIFT’s volume savings were purely gifted to the banking community. The corporate was still waiting for the benefit.

This is the struggle that has been taking place within the SWIFT community for the past decade and, to a lesser extent, still rages today.

How do you give savings to the corporate and how do you allow corporates to exploit standards, when all it does is erode margins for their current payments provider and allows the corporate to become a rate tart with easy switching to any other bank.

Tough.

The days of proprietary lock-ins are over.

SWIFT has recognised this and are ever more embracing of the corporate community for this reason.

Forget payments, transaction and messaging ... SWIFT's future is all around secure information exchange between banks, between businesses and, you never know, but one day in the future maybe even between individuals.

And banks are now scrabbling harder and harder to keep their corporate clients happy and well served for this reason.

Some of us would say, “isn’t that how it’s supposed to be? Shouldn't banks always serve their customer well?” ...

... yeah, but it hasn't been that way in the past because once you got the sucker, they couldn't get away.

But now they can and so let's look at what the banks are doing to serve their corporate clients better.

This was a question posed by Gary Wright, Director for International Payments with Royal Bank of Scotland last week at the Financial Services Club.

The evening focused upon the opportunities and issues with real-time payments and this is the innovation in corporate banking and payments that is taking place today, as we speak.

Real-time.

Real-time money movements intra-corporate and inter-corporate, intra-bank and inter-bank.

Real-time payments across borders and continents.

Real-time trade flows of information and risk.

Real-time.

That’s where the corporate money is at.

For a bank, you see, the old world of reporting as the bank wanted, when the bank wanted, how the bank wanted and what the bank wanted to report, was how it worked.

There was no incentive to leverage the information flows the bank had access to, which was a privilege. Banks have access to masses of trade data you see, but where was the incentive to tap into that data?

For many, with customers locked in via proprietary network connections that were hard-wired into back office systems, the incentive just was not there.

But today, with open networking via cloud-based systems that plug and play into SAP and ORACLE Enterprise Resource Planning suites of software, there is a huge incentive for a bank to re-engineer itself back into the corporate value-chain.

And that’s exactly what banks are starting to deliver.

So Gary joined an esteemed panel of industry payments experts, including:

- Chris Pickles, Head of Marketing for Financial Markets & Wholesale Banking with BT Global Services;

- Jonathan Williams, Strategy Director for Experian Payments;

- Martin Wilson, Chief Commercial Officer for VocaLink; and

- Tom Buschman, Chairman of TWIST Standards and CEO of EDGE.

It was an interesting debate and Gary, as mentioned, began by posing what do corporates really, really want, a-zig a-zig ah!

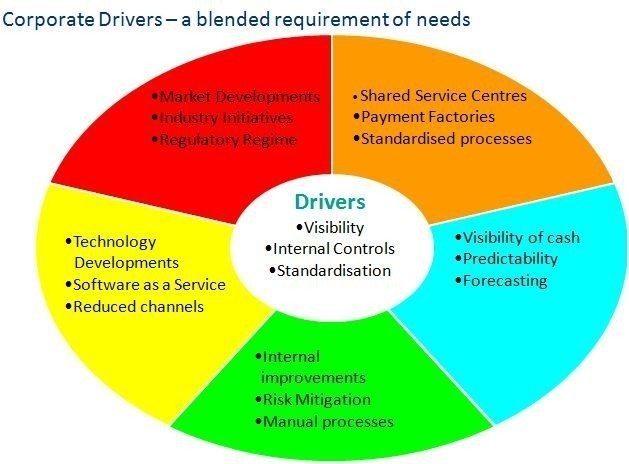

Gary answered this with a great slide. Just one slide, but a real goodie.

Here it is:

What this slide shows is the range of drivers that corporates have towards real-time services and improved delivery of services from the payments provider.

The fact is that working capital is the issue.

Without good visibility and transparency of working capital, corporates are stymied into a vacuum of ignorance.

It reminded me of a debate I had about four years ago where we talked about cash pooling and netting. One software firm had created a system that provided a real-time view of every corporate client of the bank’s cash positions globally.

With the click of button, the bank’s risk managers could see which clients were exposed where and when, and manage the situation.

The problem the software vendor had is that no bank wanted their system.

Why would a bank spend millions on a system that told them their clients were possibly exposed in real-time?

Intra-day or end-of-day would do.

That’s why the system wasn’t selling.

But guess what.

Turn that on its head and start talking about real-time cash management for corporate treasury today as an information service and guess what? You’ve got a winner.

The corporate treasurer mindful of his global financial positioning loves the idea of real-time.

And this is what banks are now buying into as a value-add service that differentiates them from the pack.

The more real-time service, the more real-time information, the more real-time movement to decrease fraud and risks, the more real-time capability to see how to improve ROI and decrease losses, the more a corporate client will love ya’.

And that’s what banks want.

Not to be loved ... but to keep their corporate client.

The other guys on the panel reinforced this view, but you have to be a member of the Financial Services Club to find out what they said.

Just to give you a glimpse however, I asked each panellist to see how they saw the future of payments and real-time at the end of the one hour panel discussion and here is what they said:

As you can see, the audience were riveted!

Anyways, the net:net on innovations in transaction services for commercial banking is that if you aren’t enriching your clients with real-time information services about their use of your bank’s services ... then you’re missing a trick because the competition is doing just that.

And by the way, e-invoicing and related innovations in supply chain management play right into that space too.

p.s. Martin Wilson articulated much more detail on this panel about the research VocaLink released at SIBOS on Faster Payments. If you want a copy, just click here.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...