As mentioned, last week was a Remittances week in Rome.

Remittances continually intrigues me as a market, especially the major focus financial institutions are now placing on this area as an opportunity. This is contradictory as those who need remittance services the most are often those who do not use banks or have bank accounts.

So there’s an anomaly there.

Nevertheless, the banks’ interests are probably something to do with the fact that there’s $375 billion worth of remittances sent around the world every year.

First, we need to consider exactly what a remittance is.

Most folks think of a remittance as money transfer from a migrant worker to their family in another country, with 14 major sending countries to 72 receiving countries according to the World Bank.

These are:

- Canada to India; Vietnam; Jamaica; Haiti

- France to Senegal; Mali; Côte d'Ivoire; Haiti; Morocco; Tunisia; India; Vietnam; China; Algeria

- Germany to Turkey; Lebanon; Serbia; India; Romania; Bosnia and Herzegovina; Croatia; Morocco; China

- Italy to India; Philippines; Albania; Romania; Serbia; Nigeria; Sri Lanka; Morocco; China

- Japan to Philippines; China; Korea; Brazil; Peru

- Malaysia to Indonesia

- Netherlands to Morocco; Suriname; Nigeria; Turkey; Indonesia; Netherlands Antilles; Ghana; Dominican Republic

- Russia to Armenia; Kyrgyz Republic; Belarus; Moldova; Azerbaijan; Georgia; Ukraine; Tajikistan; Kazakhstan; Uzbekistan; Latvia; Lithuania; Estonia

- Saudi Arabia to Pakistan; Yemen; Bangladesh; India; Philippines; Egypt; Jordan

- Singapore to Bangladesh; India; Malaysia; China; Indonesia; Pakistan

- South Africa to Swaziland; Lesotho; Zimbabwe; Angola; Botswana; Mozambique; Malawi; Zambia

- Spain to Dominican Republic; Colombia; Peru; Brazil; Romania; Ecuador; Philippines; Morocco; Bulgaria; China

- United Kingdom to Brazil; Pakistan; Poland; Bangladesh; Nepal; Sri Lanka; Philippines; India; Sierra Leone; Nigeria; Ghana; Lithuania; Uganda; Romania; Bulgaria; South Africa; Jamaica; Kenya; Albania; Zambia; Rwanda; China

- United States to Ecuador; Vietnam; El Salvador; Peru; India; Nigeria; Ghana; Guatemala; Honduras; Colombia; Jamaica; Mexico; Philippines; Haiti; Dominican Republic; Guyana; Indonesia; Brazil; Pakistan; China; Lebanon; Thailand

The primary receiving countries are India (15% of global remittances), Mexico, Philippines, China (8% each), Turkey (6%) and Egypt (5%), and the top 16 receiving countries represent 75% of all remittance receipts.

All of this is fluid however, as economic migration is predicated on economic health and, as seen recently in the UAE, if the economies falter then so does the economic migration:

“It's the great escape by Indians who've hit the dead-end in Dubai. Local police have found at least 3,000 automobiles -- sedans, SUVs, regulars -- abandoned outside Dubai International Airport in the last four months.”

Nevertheless, global remittances is big business, particularly as the traditional model of money transfer – via an agent’s office such as Western Union’s or via Hawala - is changing thanks to technology.

With half the world now able to access mobile telephones, the remittances space is being re-engineered. This was illustrated well by the rise of m-Pesa in Kenya – from nothing to 7 million subscribers in just two years making this the largest financial services in the country – which led to the announcement by Citibank of an agreement with Vodafone to emulate the success of the service worldwide.

Since then, Vodafone have linked with other providers, such as Western Union, and mobile and prepaid remittances is definitely worthy of note.

This led to an illumination for me last week, which is that it is not the transfer of money or the technology which drives this marketplace … it is how to get value from person to person.

Whether the transfer of value is via an agent, mobile telephone, card or other service does not matter. Purely the accessibility to sending value and receiving value.

In this context, the sender typically lives in a developed or growing economy – France, Germany, Italy, Spain UK, Russia, Saudi Arabia, South Africa, Japan, Singapore, Malaysia, USA, Canada – to one that is underbanked and often underdeveloped.

In other words, from countries with high density of technology access to countries with lower or poor access to technology.

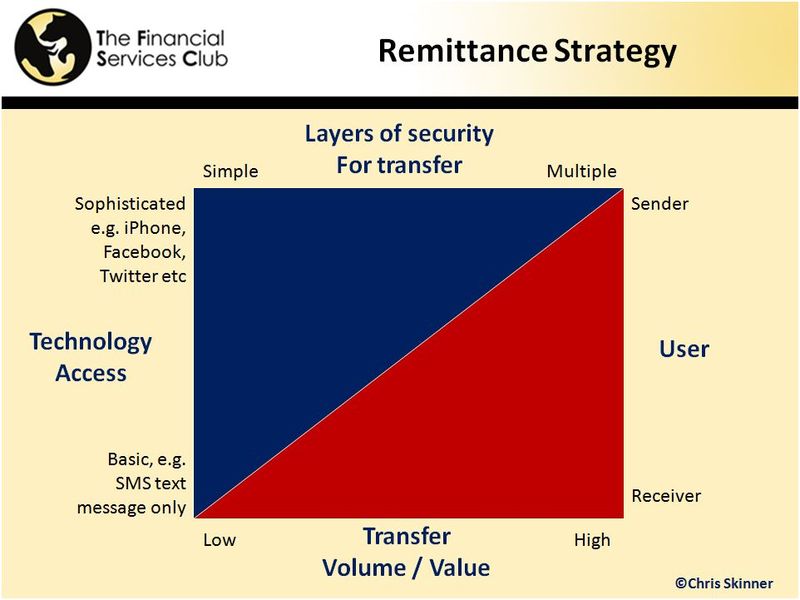

With this in mind, I felt a chart for a remittance strategy could look something like:

In other words, this aims to provide sender’s with sophisticated and ubiquitous access points to send value via any technology channel, including anything from an iPhone app to a money transfer agency … through to receiver’s being offered simple and ubiquitous access via the most appropriate channels for the culture and country infrastructure which for many will be SMS text messages and / or a money transfer agency.

Oh yes, and value could be monetary remittances, but it doesn't have to be. It might be airmiles, loyalty points for telephone or food services, or even games, ringtones and anything else that has a value ...

This is just a scribble on the back of a notepad at this stage, but may be worth fleshing out into something more substantial.

Would be interested in any views …

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...