I’ve talked about UMPay, a JV between Unionpay and China Mobile, as

well as eBank, an internet bank leader in Japan now owned by an

etailer, Rakuten Group.

This leads nicely into what is probably the most innovative bank I've

seen so far: Jibun Bank, a Japanese bank which translates into ‘my

bank’ in English.

Why is Jibun Bank an innovation?

Because it is designed purely and simply for mobile telephone access.

Jibun Bank was launched in July 2008 by the Bank of Tokyo-Mitsubishi UFJ (BTMU) and KDDI, the Japanese telecommunications carrier.

Makoto Shibata-san of the BTMU joined me in Hong Kong and talked briefly about how it works:

Jibun Bank now has around 400,000 customers.

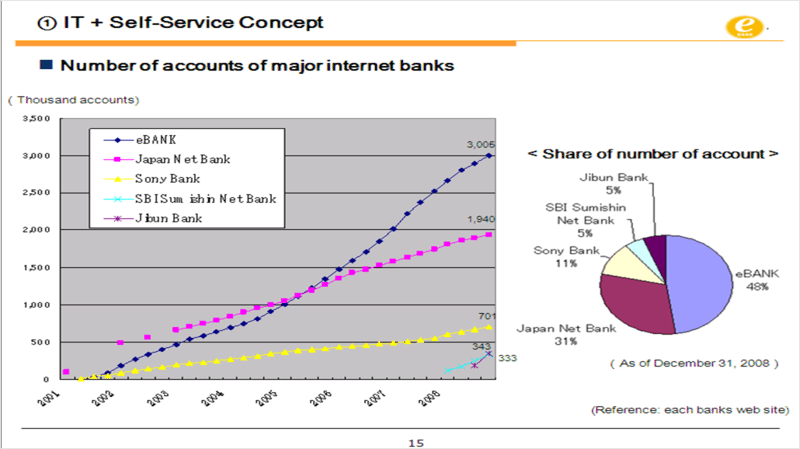

That may not seem like many, but it’s not bad for a mobile only bank. In fact, it’s better than not bad when you think the bank is only six months old and, as Saiki-san of eBank demonstrated yesterday, Jibun Bank is actually growing at quite a pace against other banks.

For example, here is one of Saiki-san’s slides (double-click image to see in larger size):

As can be seen, according to these stats, Jibun Bank has taken a 5% market share already, as has the new bank SBI Sumishin Net Bank, an Internet bank jointly established as an innovative customer-oriented new bank by SBI Holdings and The Sumitomo Trust Bank.

The difference with Jibun Bank is that it is intended for mobile access only, and only has a shell website to back it up.

The aim instead is that, through KDDI’s mobile telephone stores and BTMU’s branches, you get full service access via 24*7 telephony.

The 24-hour bank is also designed for mobile phone subscribers of KDDI's au service, allowing au users to pay for goods and services they purchase with their mobile handsets and making money transfers between au subscribers as easy as just entering the receiver's telephone number and the amount of money to be transferred into the handset.

Meanwhile, to deposit or withdraw cash, customers can use BTMU’s ATMs or those of Seven Bank and the Japan Post Bank.

And if you thought 5% market share was aggressive then that’s just the start as the banks has announced aggressive targets of 2.4 million accounts with deposits totaling ¥1 trillion (US$10 billion) by April 2010 rising to 3.4 million accounts and ¥1.5 trillion (UD$25 billion) the year after.

That would represent over half the online market for banking.

And this is not just important to BTMU but also to KDDI, as they compete with NTT DoCoMo and Softbank to find new customers and diversify.

This means that the model of this bank is different to traditional deposit takers and lenders, as Jibun Bank expect to generate half their income from fees and the other half from investments on deposits.

This places the business model closer to the 7-Eleven convenience store style banking of Seven Bank.

Between telco banks (UMPay and Jibun Bank) and retailer banks (Seven Bank), along with yesterday's story about eBank being owned by an etailer (Rakuten), the cross-industry partnerships and joint ventures we are likely to see in banking grow by the day.

If you want to know more about Seven Bank, then watch the video of Takashi Anzai, President of Seven Bank Japan.

If you want to know more about Jibun Bank, a few details from the press release at its launch in July 2008 below, which pretty much says it all:

Jibun Bank Corporation started accepting applications from customers for new accounts in July 2008, with full customer services via mobile phones (au, NTT DoCoMo, and Softbank Mobile), the Internet (PCs), and the telephone (IVR/operator).

At the same time, KDDI Corporation and the Bank of Tokyo-Mitsubishi UFJ have started marketing and opening accounts for Jibun Bank as bank agents.

Making the most of mobile phones, Jibun Bank is striving to become a financial institution with top customer satisfaction - a "personal bank for each individual customer" - providing high-quality financial services that are both convenient and secure.

Method for opening an account

When opening an account at Jibun Bank, customers don't have to register their seal and signature. Applications for new accounts are accepted in various formats including "quick account opening" using the Jibun Bank Book software, a specialized software making it even easier to access Jibun Bank services, "mobile phone order" through the mobile-phone Internet site, "computer order" through the Internet website, and "mail order" through the land mail.

This is very similar to eBank's account opening process described yesterday.

Customer Channels

In addition to Jibun Bank's own channels through mobile phones, Internet (PCs), and telephones, KDDI and the Bank of Tokyo-Mitsubishi UFJ provide customers with access to Jibun Bank accounts as bank agents through their stores and branches.

Products and services

The following products and services are being provided with the launch of customer services:

- Yen deposits - ordinary and time deposits.

- Transfers - mobile phone number transfers (some services require au Information Link services and Jibun Bank Book software) and bank account number transfers.

- ATM transfers - deposits, withdrawals, and balance inquiries, which can be carried out at Bank of Tokyo-Mitsubishi UFJ, Seven Bank, and Japan Post Bank ATMs. Charging electronic money Edy (some services require au Information Link services and Jibun Bank Book software).

In the future, additional services will gradually be added including foreign-currency-denominated deposits, credit card loans, credit cards, financial product intermediation, and sales of insurance.

Security functions

Numerous safety functions are available including ATM Lock and Computer Lock (both requiring au Information Link services), and transaction notification through mobile phone text messages so that customers can use the convenient Jibun Bank with peace of mind.

In addition, au Information Link Service increases the convenience and safety of mobile phone banking by linking customer's au contract information with bank transactions after Jibun Bank receives the consent of the customer.

This service further raises the level of security through various functions, such as making it impossible to access mobile phone banking (including the Jibun Bank Book software) with a mobile handset other than the registered one.

Payments

The Jibun Bank Payment service makes it possible to easily and quickly make payments for shopping and auctions on EZweb, including au Shopping and au Auctions. The number of Internet shops that this can be used with is gradually expanding.

Launch campaign

With the launch of Jibun Bank, a campaign offered customers opening new accounts up to ¥1,500 (US$15) in presents. Customers opening a new account receive ¥500 ($5), and customers applying for the au Information Link service receive an additional ¥1,000 ($10) present.

The Jibun Bank Information Counter

Jibun Bank also launched the Jibun Bank Information Counter at its headquarters in Shibuya, near the Bank of Tokyo-Mitsubishi UFJ Plus Shibuya Branch Office and the KDDI store. At the Jibun Bank Information Counter, specialised staff are pleased to provide information on Jibun Bank products and services with hands-on demonstrations and pamphlets as well as taking applications for new accounts.

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...