Interesting discussions going on about the latest social media craze, Twitter.

As the site describe themselves: "People are eager to connect with other people and Twitter makes that

simple. Twitter asks one question, 'What are you doing?' Answers must

be under 140 characters in length and can be sent via mobile texting,

instant message, or the web."

I Twitter through various feeds as do around seven million other folks, and it is a great short message service for those who want to lifestream (social networking phraseology for sharing one's life digitally).

So Twitter is basically an easy way of linking your internet and mobile lifestyle with easy updates.

The site has been around since March 2006 and shot to fame in the last few days because the first photograph of the Hudson River US Airways crash was broadcast on Twitter, via a user’s upload from their mobile phone.

I'm talking about it today

because banks are vulnerable to identity theft issues via Twitter, just

as they are via Facebook and other social media.

First, there are the obvious user issues with identity, e.g. I know what you did last summer and all that.

More importantly however, is the ability to use Twitter to steal a bank's identity.

What?

Sure.

Right now, I can point to a few banks that are using Twitter to improve customer communications, such as Wachovia and Bank of America, along with a few social finance sites such as SmartyPig (check it out).

But most banks are not Twittering yet and, for this vast majority, they should own their Twitter name at the very least or it might get hijacked.

Some banks have secured their name, such as Wells Fargo (isn't that Wachovia?) who are holding the Wells Fargo Twitter name just in case.

Some may or may not be secure, such as Citi and their variations Citigoup and Citibank.

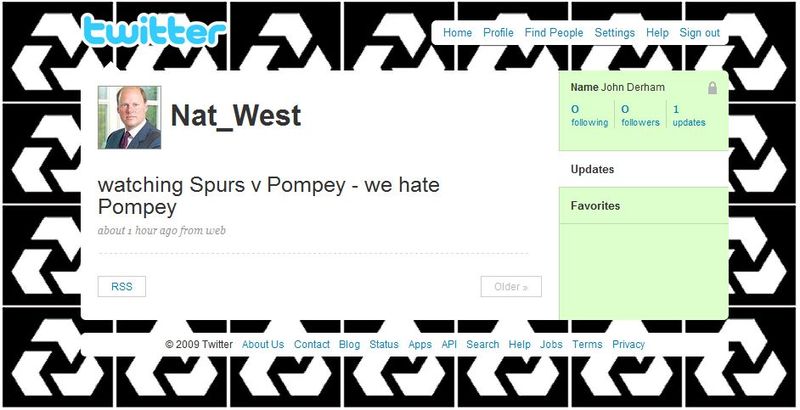

Whilst a few are obviously fake, such as JPMorgan's and Nat_West (which a friend of mine set up whilst we watched the football match yesterday):

What this means is that banks must be careful about Twitter as it could be as easy to undermine a bank's brand here as the old days of the Internet Wild West, when folks used to register domain names in the hope of multimillion dollar payouts by firms to get them back.

Wouldn't you feel like a bunch of tweets if that happened?

Chris M Skinner

Chris Skinner is best known as an independent commentator on the financial markets through his blog, TheFinanser.com, as author of the bestselling book Digital Bank, and Chair of the European networking forum the Financial Services Club. He has been voted one of the most influential people in banking by The Financial Brand (as well as one of the best blogs), a FinTech Titan (Next Bank), one of the Fintech Leaders you need to follow (City AM, Deluxe and Jax Finance), as well as one of the Top 40 most influential people in financial technology by the Wall Street Journal's Financial News. To learn more click here...